Mutual Banks Act, 1993 (Act No. 124 of 1993)RegulationsRegulations relating to Mutual BanksChapter II : Risk-based Returns and Instructions, Directives and Interpretations relating to the completion thereof20. Income statement |

| (1) | A mutual bank shall complete the form DI200 in accordance with such instructions or requirements as may be determined or directed in writing by the Authority. |

[Regulation 20(1) substituted by section 6 of Notice No. 7414 of GG54593, dated 29 April 2026 - effective 1 May 2026]

Line item number

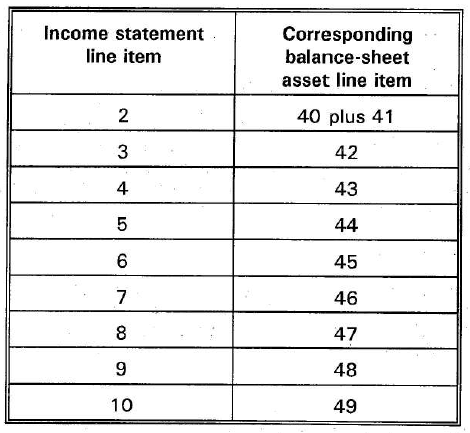

| 1. | Interest income from loans and advances |

The items listed in the income statement under this heading shall reflect interest income in respect of the corresponding asset items listed in the balance sheet, excluding unearned finance charges (that is finance charges due but not yet accrued), as follows:

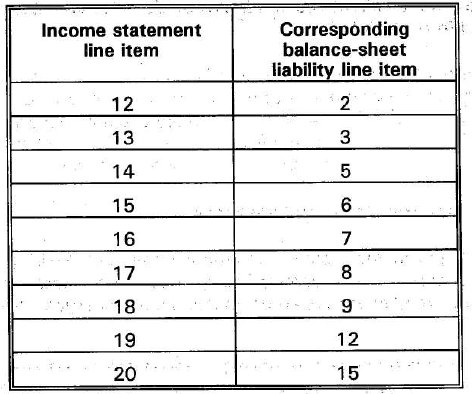

| 11. | Interest expense in respect of deposits and loans received |

The items listed in the income statement under this heading shall reflect interest expense in respect of the corresponding liability items listed in the balance sheet, excluding deferred finance charges (that is finance charges due but not yet accrued), as follows:

| 37. | Transaction-based banking-related fee income |

This item shall include all non-interest income earned as a direct result of any service rendered by the reporting mutual bank at a fee that is levied on the basis of a standardized tariff. Typically, this includes fees levied in respect of services relating to money transmission. (This item shall include fees levied i in respect of off-balance-sheet transactions, but excludes interest income.)

| 38. | Knowledge-based fee income |

This item shall include all income earned as a result of any service rendered by the reporting mutual bank at a fee that is negotiated in the case with a client. (For example, the bulk of the income from corporate finance activities of a mutual bank will fall under this item.)

| 40. | Staff |

This item shall include all salaries, wages, fringe benefits (the amount of which is computed either in accordance with the provisions of the Income Tax Act, 1962, or on the basis of opportunity cost), the institutions contributions to pension and provident funds, medical schemes, and all other costs directly related to the staff complement.

| 56. | Gross-up adjustment |

Where a reporting mutual bank has reported a tax-exempt amount against any of the aforegoing items at a notional pre-tax value, the relevant contra entry shall be reflected under this item.

| 61. | Reserves - Transfers to |

This item shall include all transfers to reserves, including the creation or increase of a taxation equalisation reserve.

| 62. | Reserves - Transfers from |

This item shall include all transfers from reserves, including the utilisation of a taxation equalisation reserve.

[Deleted] Form DI200 - Directives and interpretations for completion